MALAYSIA’s economic growth in the past 10 years has been fuelled by consumer and government spending. This Special Report explains why it is now crucial for the country to switch the engine of growth to more efficient, private sector-led investment into the sectors that will create higher-income jobs and greater economic value. To achieve this, a major structural overhaul of the economy, including regulations, will be necessary.

The global economy in 2020 is projected to fall into the deepest recession since World War II, as stringent lockdown measures to contain the Covid-19 outbreak caused an abrupt halt to almost all economic activities across both the developed and emerging-developing worlds.

According to the World Bank, gross domestic product among developed economies will shrink 7% this year while that of emerging and developing nations will drop by 2.5%, the first collective contraction in at least six decades.

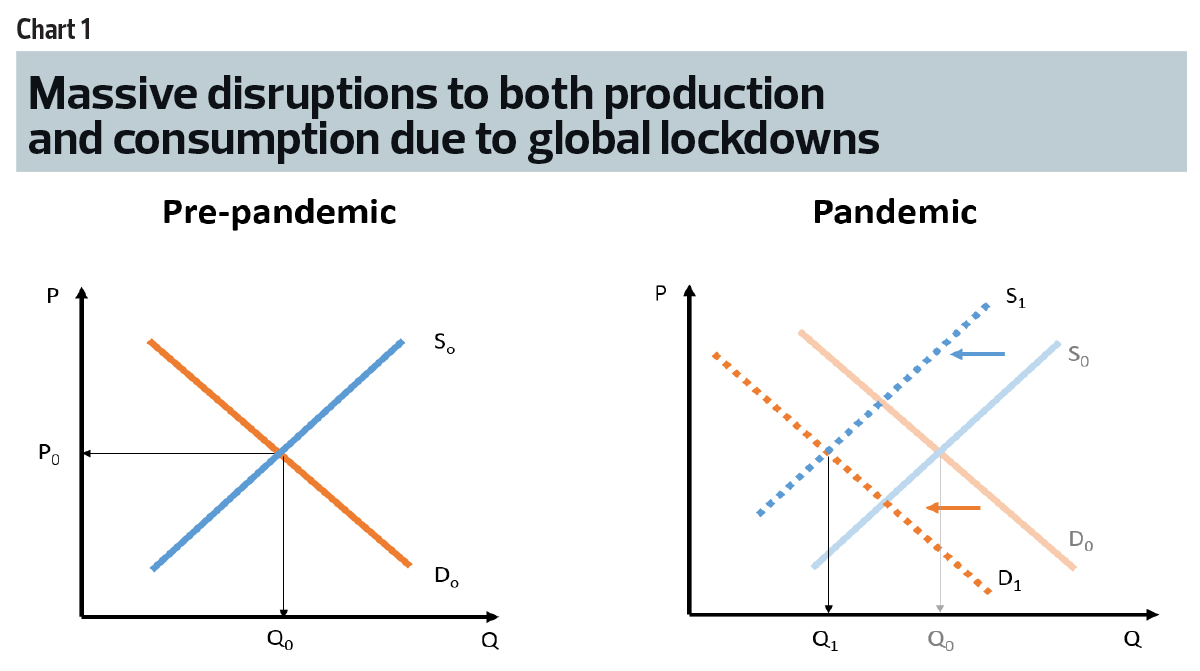

The restrictive movement measures resulted in huge unemployment, disruptions to global supply chains and may have tipped millions back into poverty. There were massive distortions to both the demand and supply sides of the economic equation (see Chart 1).

Central banks and governments have reacted swiftly to mitigate the economic impact through the injection of unprecedented amounts of liquidity into the global financial system and huge fiscal stimulus packages worth trillions of dollars.

The initial measures were focused on protecting productive capacities during the lockdowns — for instance, loan moratoriums for businesses and households as well as government/central bank loans-grants — and wage subsidies to prevent mass unemployment. Emergency benefits for the temporarily jobless and direct cash handouts were crafted to protect people’s livelihoods.

Nevertheless, we should expect a wave of business failures over the coming months, especially micro and small and medium enterprises (SMEs) suffering from insufficient cash flow and limited access to bank loans. Despite economies reopening, demand remains well below pre-pandemic levels and will only gradually normalise.

Every company, big or small, is going to be very cautious in terms of hiring and new investments, and is more likely than not to continue cost-saving measures as well as limit dividends and share buybacks to conserve cash. That means unemployment will stay elevated for some time.

In short, the worst may be over but economies are going to require a lot of help to fully recover from the shock.

As such, globally, both monetary and fiscal policies will remain expansionary.

Major central banks of the developed world — including the US Federal Reserve, European Central Bank, Bank of England and Bank of Japan — are all in on quantitative easing and near-zero or negative interest rates. Interest rates are going to stay very low for the next two years, at least.

By aggressively cutting the price of money, they are pushing banks to lend and businesses to invest, to take on more risks. Liquidity is also driving prices for almost all asset classes — stocks, bonds and commodities such as gold — higher. This should, in turn, create the wealth effect, which will further spur the recovery in consumer spending.

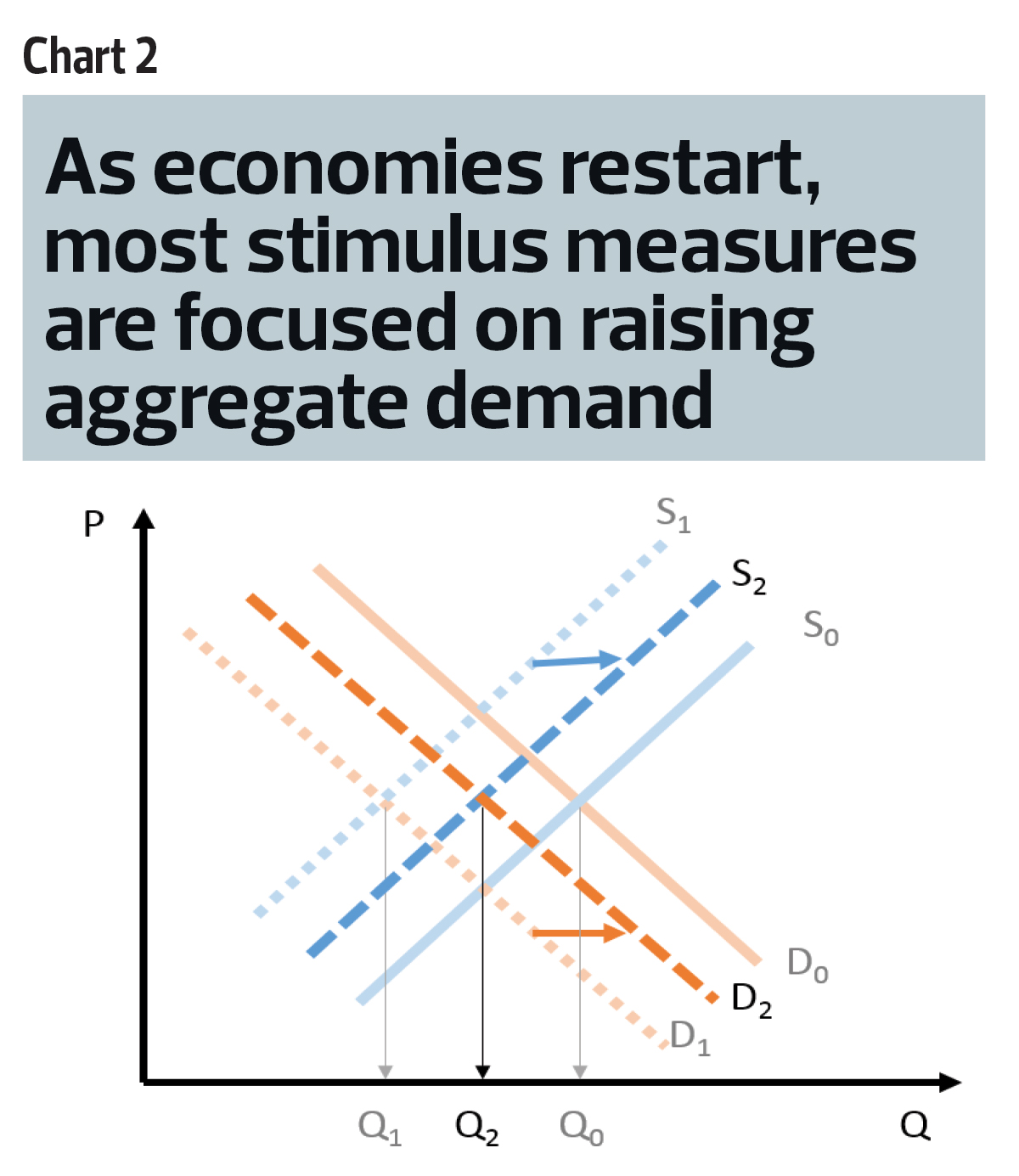

The traditional Keynesian macroeconomics response to recession is to stimulate aggregate demand, through tax cuts and fiscal spending (see Chart 2).

For example, in the US, the Trump administration is preparing a US$1 trillion ($1.38 trillion) infrastructure package. The German government agreed to a EUR130 billion ($208.54 billion) stimulus package that includes a temporary reduction in the value-added tax rate, rebates for electric car purchases and cash handouts for families.

We think Malaysia should take a higher-level approach. Rather than only focusing on stimulating aggregate demand (consumption), we should take this opportunity to also execute an economic structural reset. As Winston Churchill once said, “Never let a good crisis go to waste.”

What we would really like to see is a pivot from consumption to production, instead of pushing growth from more consumption and spending. It is time to push growth by raising production and efficiency, generating higher income and employment.

In simple layman’s terms, this means extracting more output from proportionately less resources. How? By transforming the existing structure-ecosystem of industries, making processes more efficient by leveraging technology and removing friction and leakages, improving ease of doing business and getting approvals as well as ensuring a more transparent and competitive domestic marketplace.

All of the above would effectively lower the average costs of production (price) and thereby the cost of living for Malaysians — while also enhancing Malaysia’s competitiveness in the global market — and reinvigorate investments that will raise employment, disposable incomes, purchasing power and, finally, our standard of living.

A little background on Malaysia’s economic evolution

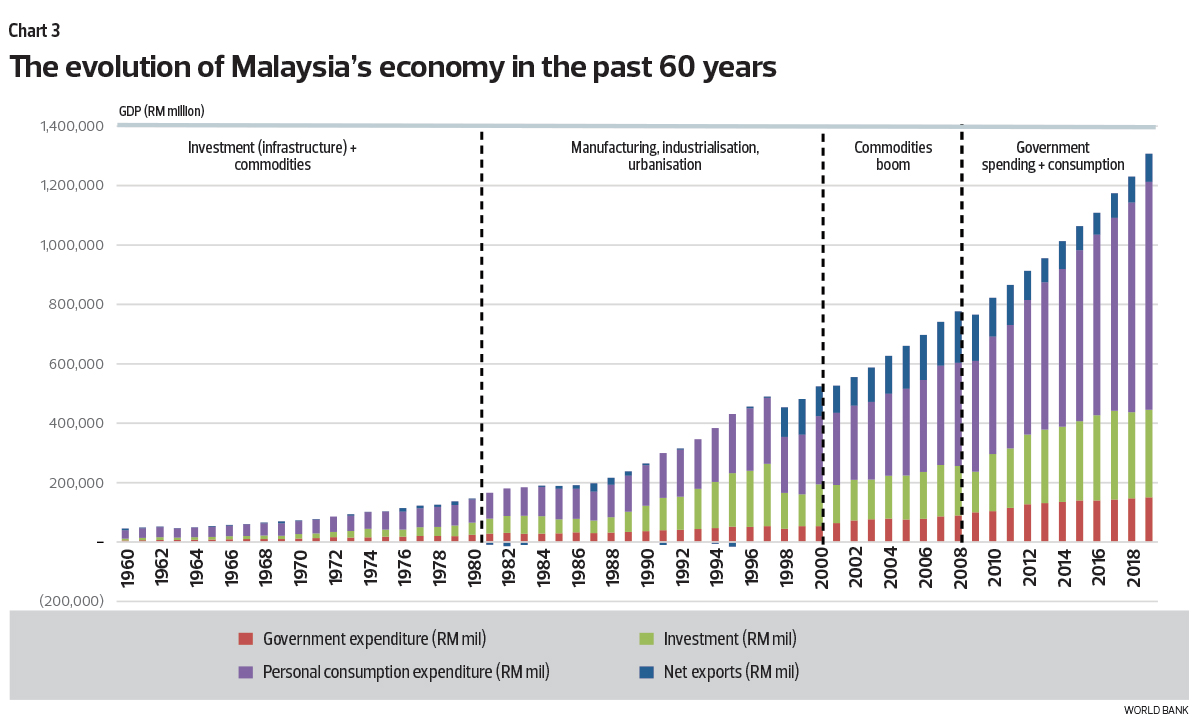

Before we go into more details on the how and why we believe the best — and only — way forward is to pivot from consumption to production, it is useful take a look back at the evolution of the Malaysian economy over the last 60 years (see Chart 3).

In the earliest years following the formation of Malaysia, we were primarily an agrarian economy and the key exports then were rubber, tin, logs and timber, mainly in the form of raw commodities. Investments were primarily for basic infrastructure and development of the agriculture and mining sectors.

The first major transformation came in the 1980s, when Malaysia pivoted from a resources-based economy to one based on manufacturing. Exports shifted to manufactured goods such as electronics and electricals. Our industrialisation programme was driven by foreign direct investments from multinational companies. This was accompanied by rapid urbanisation and gains in per capita incomes as the standard of living improved significantly.

The country’s growth progression was interrupted by the severe economic shock from the Asian financial crisis (AFC) in 1997/98. In the ensuing years, investments fell sharply as the financial system and businesses grappled with a debt burden and overcapacity while capital controls affected foreign capital inflows.

At the turn of the century and for the better part of that decade, GDP growth downshifted but fortuitously, net exports grew strongly, boosted by the global commodities boom. Prices for our main exports, crude oil and crude palm oil, surged to record-high levels. The commodities super cycle ended in 2008 with the onset of the global financial crisis (GFC).

The Malaysian economy underwent yet another major transition through the 2010s. The investment-export-driven model of the previous three decades gave way to one that is now underpinned by consumption and government spending, focused on mega infrastructure projects.

Heading into the 2020s, it is clear that Malaysia can no longer rely on this consumption-driven model to drive future economic growth. Why do we say this?

Consumption-driven growth model no longer a viable option

As mentioned above, the majority of countries in the world are focused on stimulating aggregate demand in the aftermath of the pandemic. This is the traditional response. For Malaysia, however, this path is full of pitfalls.

Aggregate demand = Consumption + Investment + Government + Net Exports

The government has actively encouraged domestic consumption as the key driver of economic growth for the better part of the past two decades.

From a macro perspective, this is a natural progression for most economies as they develop — from agriculture to industrialisation and ultimately transitioning to a services-based economy supported by consumer spending. In the US, consumer spending accounts for 70% of economic activities.

Back on the home front, consumer spending accounted for 43.8% of GDP in 2000, gradually rising to nearly 60% in 2019. So, the strategy worked — from a limited perspective.

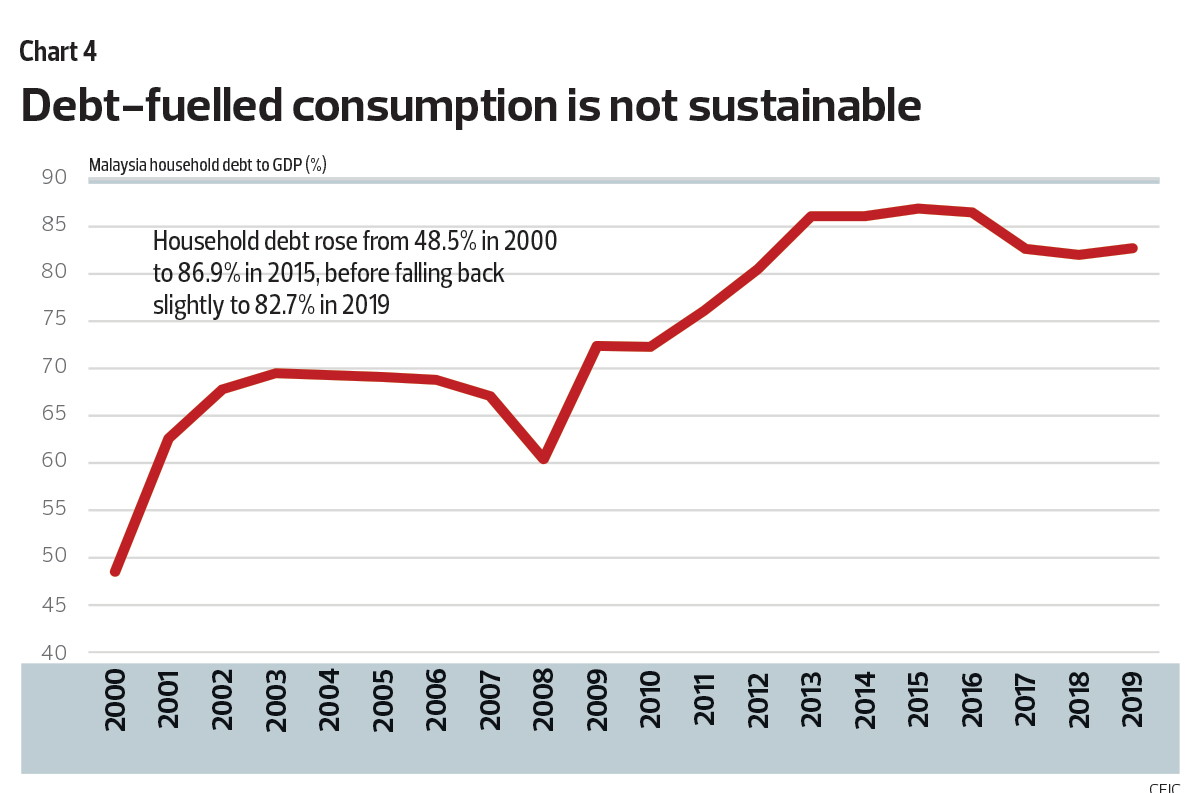

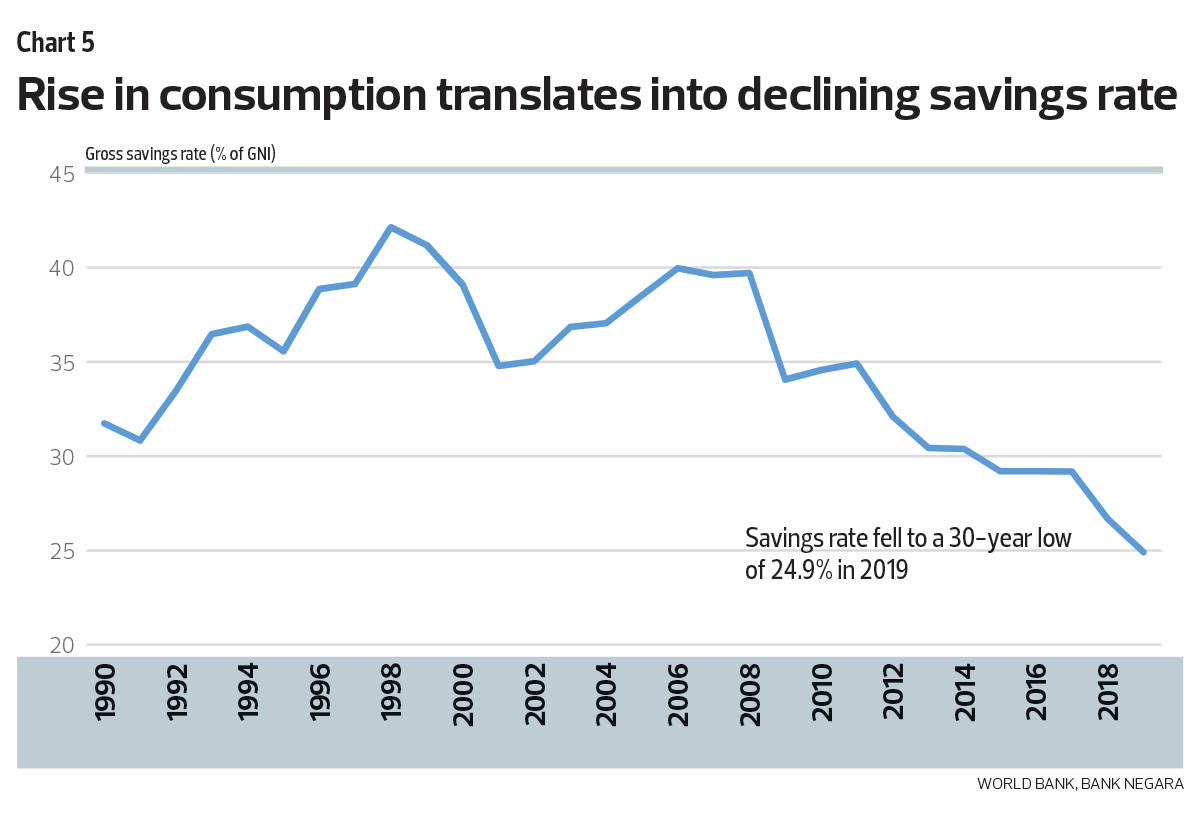

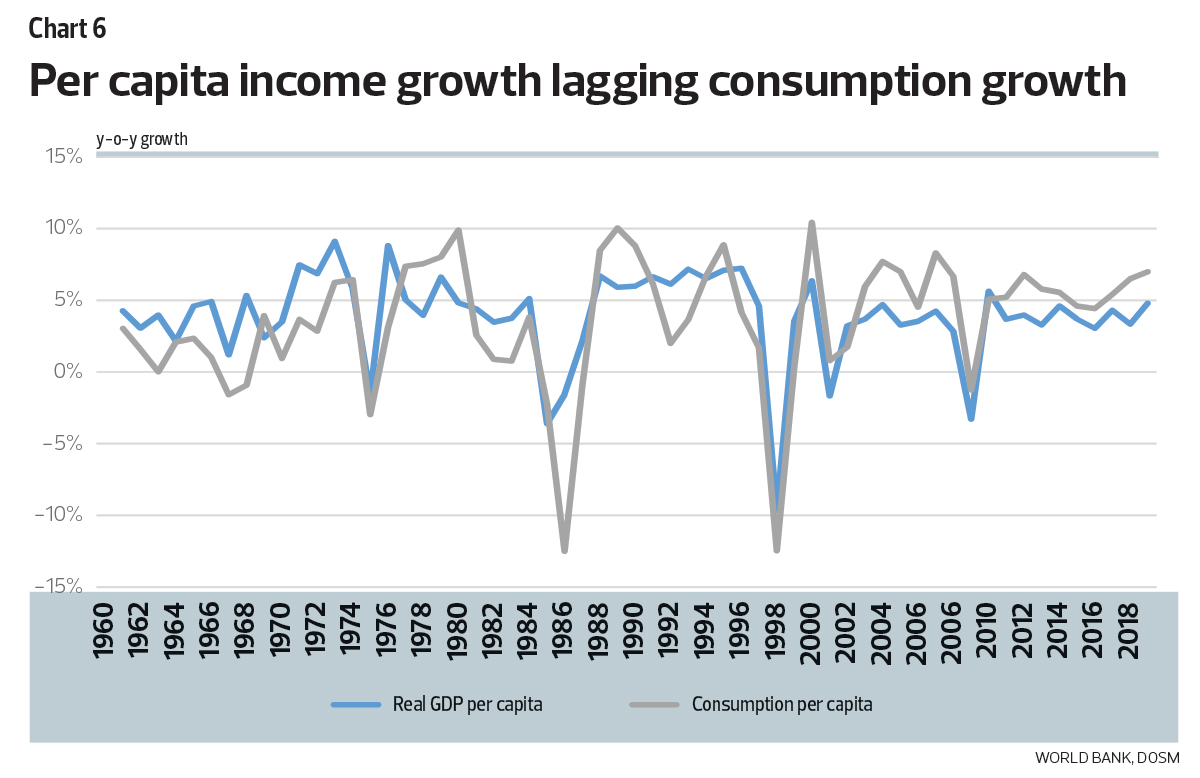

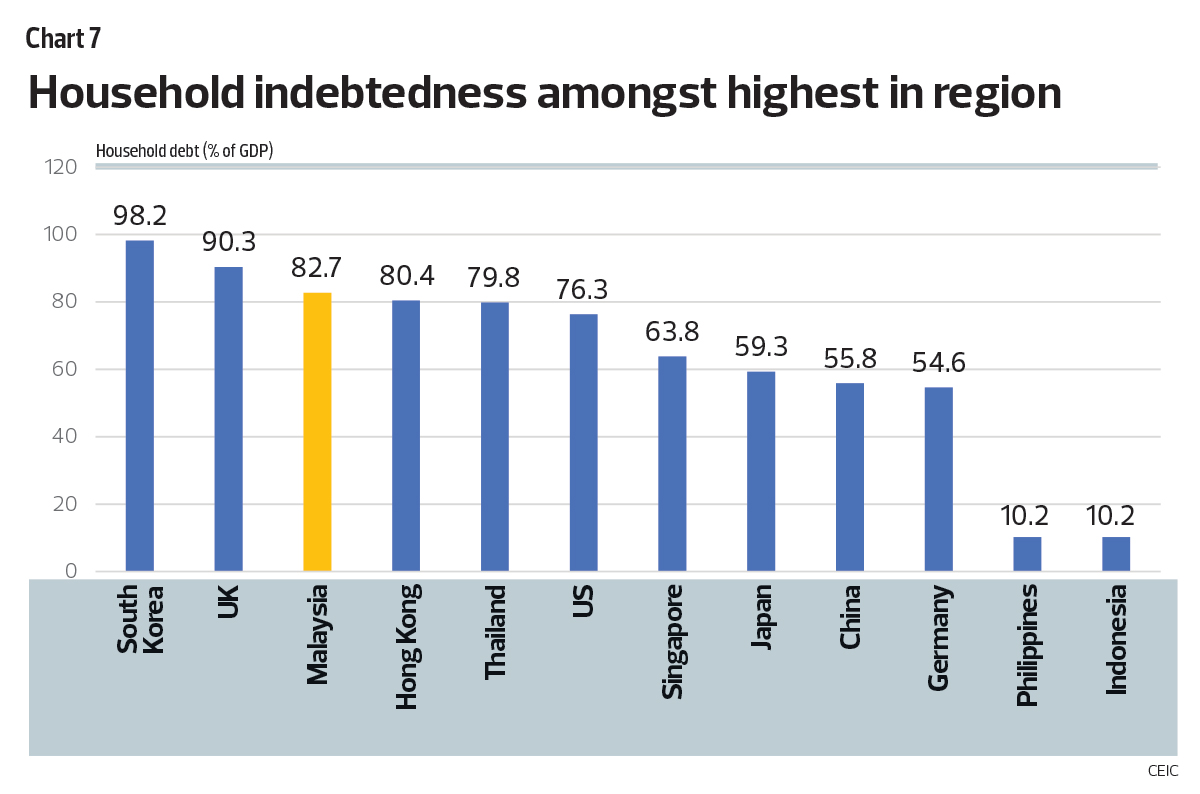

The trouble is, per capita income growth has consistently lagged consumption growth since 2000. This is best reflected in the sharp rise in household debt and corresponding decline in savings rate. Our household debt as a percentage of GDP is now among the highest in the region (see Charts 4 to 7).

In other words, we have been living beyond our means — taking on more and more debt to maintain our lifestyles at the expense of the future. Clearly, this is not sustainable. The average Malaysian has limited savings to meet emergency needs and even less for retirement.

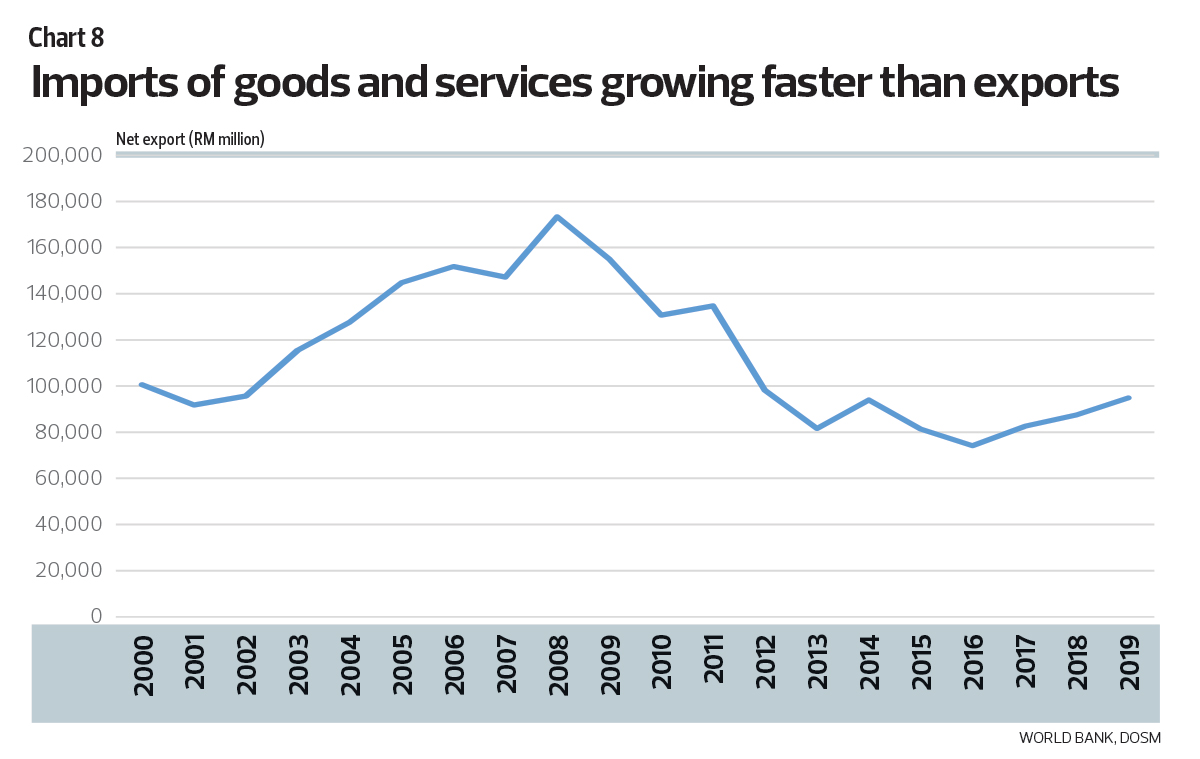

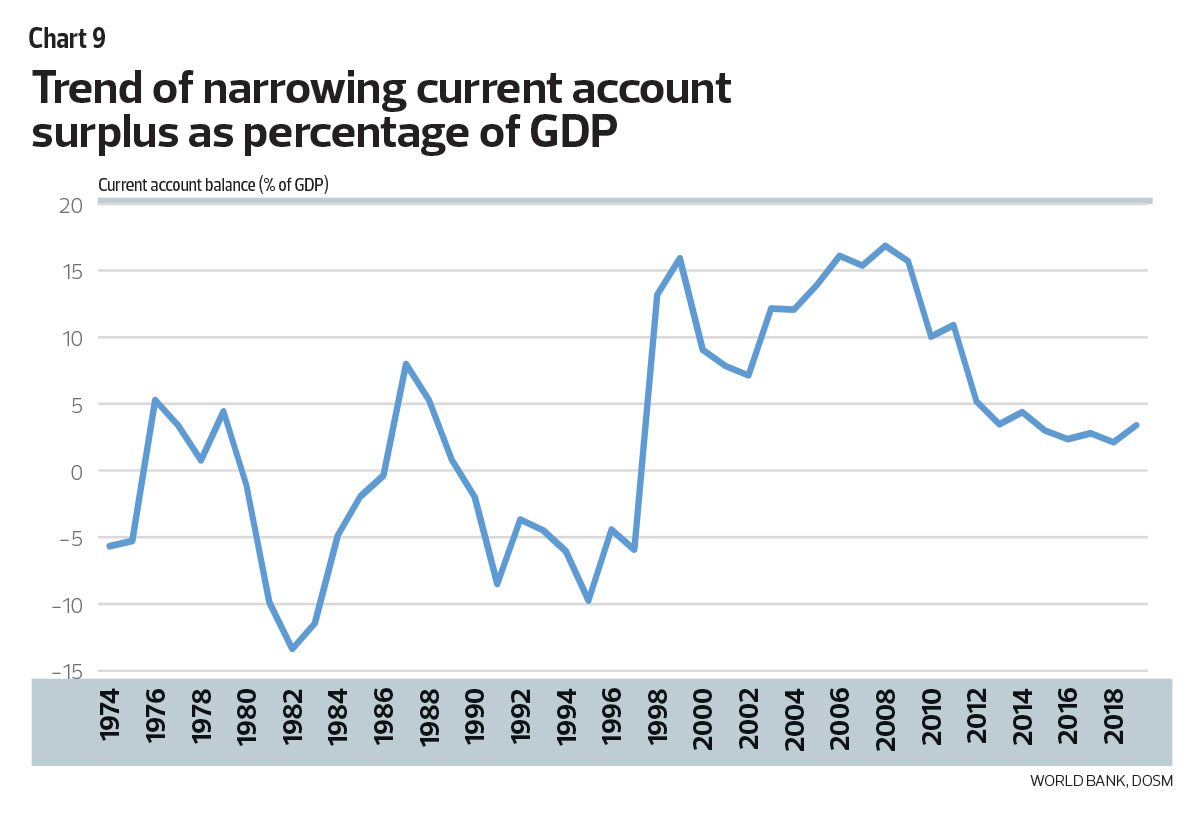

The commodities boom in the early 2000s propelled exports — and our current account surplus — higher. But after the bubble burst, surplus as a percentage of GDP has consistently declined as imports growth exceeded exports. The domestic consumption boom contributed to this decline, as consumers spent on imported goods and services, such as travel expenses (see Charts 8 and 9).

With the disruption in supply chains and global economic recession owing to the pandemic, exports are likely to decline further in the near to medium term. Prices for crude oil and crude palm oil, too, have fallen sharply and are expected to stay low for some time. Thus, we cannot depend on exports alone to lift the country out of recession.

In fact, Malaysia’s current account may fall into deficit, for the first time since the AFC. If so, this means that we are looking at twin deficits — the current account deficit and government budget deficit. Left unchecked, such a situation will create downward pressure on the ringgit.

This situation also restricts the government’s ability to implement large fiscal stimulus packages, which were already limited at the outset of the pandemic owing to years of profligate spending. The drop in global oil prices further cuts into government revenue while tax revenue will fall in line with the economic downturn.

Unlike the US — and its unique status as having the global reserve currency — a much smaller economy such as Malaysia does not have the luxury of running huge deficits without (much) consequences.

A laser focus on stimulating demand (without raising supply) could also lead to price increases, which would further inflate the cost of living. The average Malaysian is already struggling to cope with the relentless rise in living expenses.

For all of the reasons detailed above, it is clear that the old and tried — easy — strategy of pushing consumption to grow the economy is no longer a viable one. We have exhausted this option, at least for the immediate future.

Moving from consumption to production

Consumption could be a sustainable driver for economic growth in the longer term. But first, we need to raise people’s disposable incomes and lower the cost of living — so that consumption growth is sustainable, without having to resort to higher and higher debts.

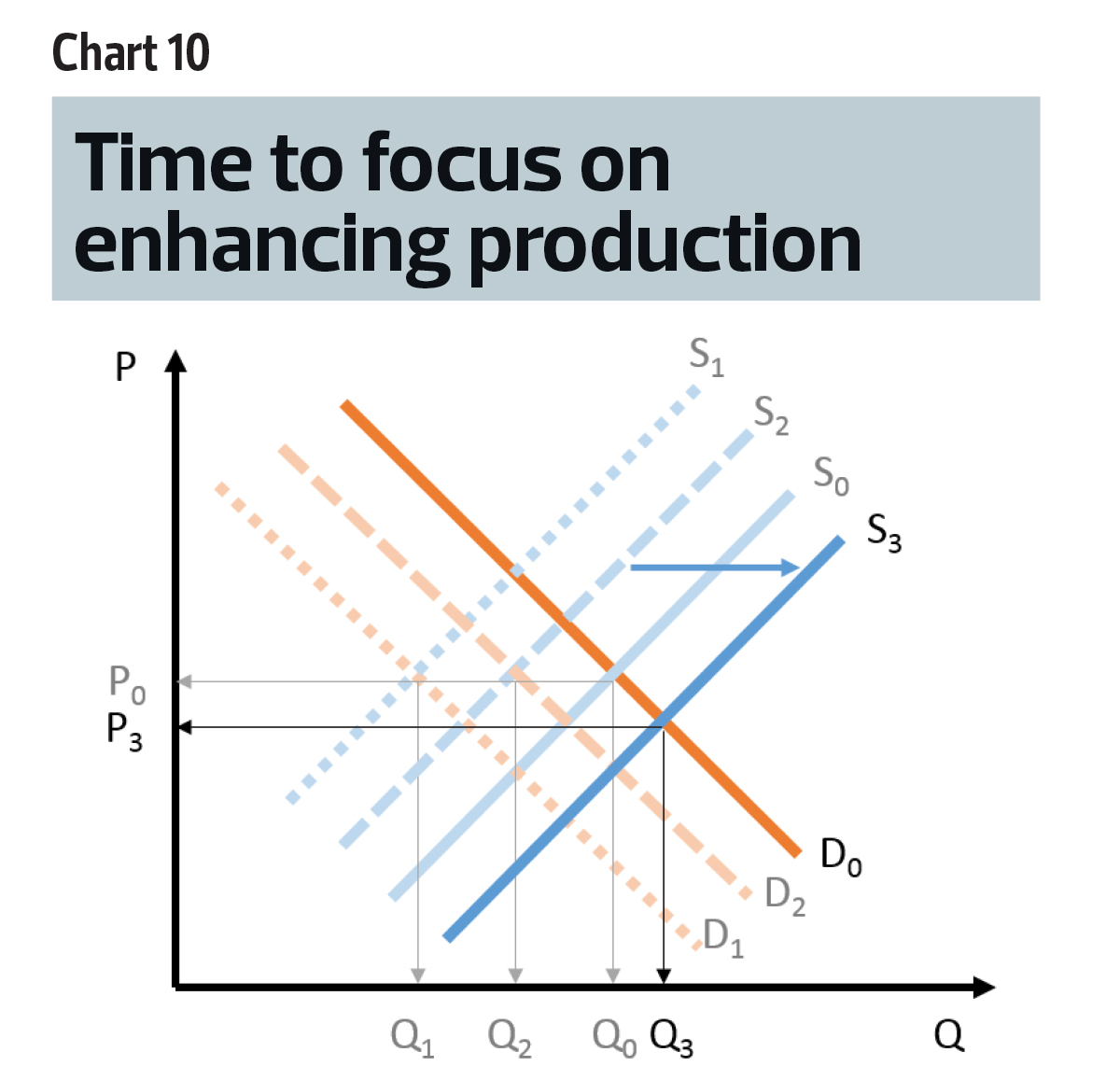

We will not pretend to have all the answers. However, we know that addressing the supply side of the equation today is the right path forward (see Chart 10).

Reinvigorating investments as key driver for sustainable growth

Part of the answer has to lie with rejuvenating investments. And by that we mean investments in productive assets as well as in intangibles — research and development (R&D), innovation, technology, education and training — all of which will enhance future productivity, create higher-paying jobs and lift overall disposable incomes in the country.

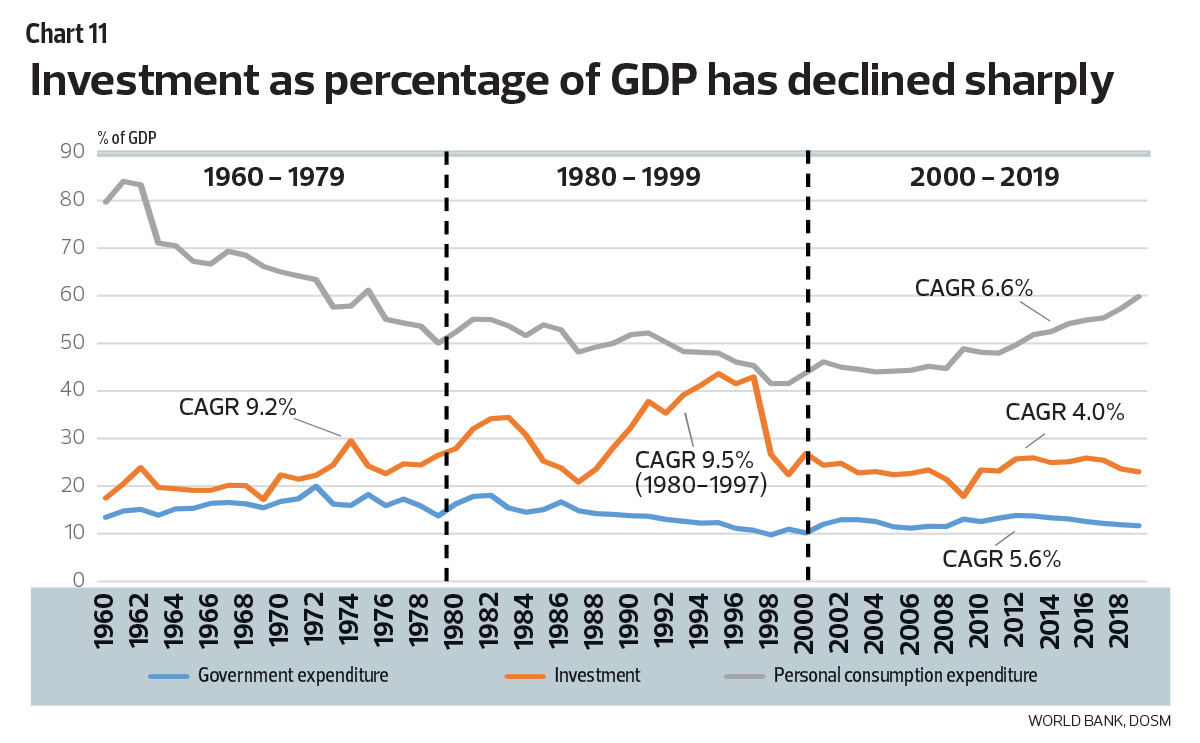

Investment as a percentage of GDP has declined sharply since the AFC, when the drivers of economic growth shifted to consumption and, to a lesser degree, government spending (see Chart 11).

Between 2000 and 2019, the compound annual growth rate (CAGR) in investments slowed to 4%, on average — below GDP growth of 4.8% — and far below that for government spending (5.6%) and consumer spending (6.6%).

This trend is in sharp contrast to the previous decades, when the key growth driver was investments. Investments grew at a CAGR of 9.5% between 1980 and 1997, and 9.2% from 1960 to 1979.

Incidentally, this shift also corresponds with a period when per capita income grew at a much slower pace compared with previous decades, albeit from a larger base.

Investing in the ‘right’ sectors

In short, moving forward, Malaysia must return to an investment-driven economic growth, a strategy that has served us well in the past. That said, we must also learn with the benefit of hindsight.

For instance, back in the 1980s, Malaysia’s government-led industrialisation plan included a focus on capital-intensive heavy industries such as auto, steel and cement. These are sectors in which we do not have a strong competitive advantage and economies of scale owing to a lack of technological knowledge and limited population size.

Many survived only on the basis of rent-seeking, where high prices and limiting imports created higher costs to other businesses and individual Malaysians.

Furthermore, it is no secret that Malaysia has failed to capitalise on our early manufacturing success and move up the value chain. This is a fact well supported by evidence, from data and surveys conducted by various institutions, including Khazanah Nasional and Bank Negara Malaysia.

Our manufacturing base has mostly languished in the cookie-cutter assembly-line type. And in the absence of sufficient spending on R&D and proprietary intellectual property, productivity stagnated.

In not moving up the value chain, we have become overly dependent on cheap, low-skilled foreign labour, producing low value-added manufacturing goods. At this level, we are competing against other less-developed countries such as Vietnam, Laos and Myanmar, where labour is abundant and starting wages are low.

To maintain competitiveness within this low value-added, labour-intensive market segment, Malaysia too has been forced to cap its wages. As a result, income per capita growth slowed.

Competition in the global market and a rise in other operating costs resulted in falling profit margins for businesses — leaving less and less for reinvestments. This has become a vicious cycle.

The pandemic crisis is the opportunity for a great reset. Not only must we re-emphasise investments as the key driver of growth, they must be the “right” type of businesses.

Private sector-driven investments the answer

Again, we do not presume to know exactly what are the best industries and businesses to be in. If we do, we would be rich! We can venture some guesses in broad strokes — they must involve technological upgrading, manufacturing of greater complexities and with deeper domestic linkages, higher value-added and knowledge-based services industries and industries with a high multiplier effect.

Fortunately, Malaysia has many far more intelligent and capable entrepreneurs who do have the answers. In short, future investments must be driven by the private sector.

The government has a very important role and that is to be the catalyst and facilitator — to provide a regulatory environment that supports innovation and attracts private investments, foreign and domestic, and removes friction for businesses to operate efficiently.

This is all the more crucial now that there is intense competition for investment (FDI) dollar — the investment strategy is being pushed by almost every other country in the world to boost their recoveries even as domestic policies take on a greater nationalist tone.

Transparent framework to minimise friction for businesses

Based on the results of various surveys, the two biggest drawbacks of investing in Malaysia are the levels of red tape and corruption.

To improve the ease, and lower the cost, of doing business, the government can start by simplifying and streamlining procedures for its interactions with the private sector.

Most existing processes can be migrated online, which would not only be faster and convenient but, more critically, transparent and consistent. A clear and transparent process will remove rent-seeking and corrupt practices, which only sap the country’s resources and discourage genuine investments.

In fact, integrating the many services among public utilities, municipalities, state and federal governments and the people into one common nationwide digital platform would lead to greater convenience and timeliness (and therefore, compliance), reduce the administrative burden, duplication and costs, and enhance overall productivity.

Injecting confidence with less conventional measures

One of the biggest obstacles to investing in the country now is the lack of confidence, given the political uncertainties and years of built-up trust deficit in the public sector. The government must address this issue head on.

One possibility is for the government to underwrite the debt servicing on select high-impact investments, if pre-agreed milestones — say, GDP or banking sector loan growth targets — are not achieved within a specific time frame.

This would give entrepreneurs the confidence to plough money into new investments while avoiding the moral hazard of promising returns without downside risks. The businesses-projects still have to succeed on their own merits against a positive macroeconomic backdrop.

This is but one suggestion. We are confident the combined brainpower of the private-sector entrepreneurs, economists and technocrats at the Ministry of Finance and Bank Negara will surely come up with many more viable propositions. The key is to inject confidence in the country and cultivate a dynamic private sector within a competitive market structure.

Productivity beyond physical assets

Enhancing productivity goes beyond physical investments and infrastructure. It is also about getting the most out of every ringgit of investment in productive capacities. Clearly, a rapid and committed transition to the digital economy is one key component.

To fast-track Malaysia towards a digital economy, the country needs reliable high-speed broadband and 5G connectivity nationwide — at affordable prices.

A common shared infrastructure — such as fiberisation and submarine cables, data centres and cloud infrastructure — with universal access will avoid unnecessary capex for network duplication, which only serves to raise overall prices for the people.

Next, the government must undertake the push for all micro and SMEs to get on board this digital transformation — on both the front and back-end of their businesses. Ideally, there will be a national platform to coordinate all the policies and programmes to ensure maximum efficacy.

The pandemic has highlighted the importance of e-commerce, which can significantly expand the addressable market (domestically, regionally and globally) for businesses.

Necessity during lockdowns has onboarded many consumers, including the less digitally literate older generation. How many of us actually bought groceries, fresh fruit and vegetables online pre-pandemic?

Most micro and small businesses that had previously neglected this sales channel too have realised the benefits from the expanded market, sales effectiveness (say, via social media) and cost efficiencies.

On the back end, businesses can improve efficiency and productivity — for human resources, IT, accounting and finance, procurement, inventory, supply chain, sales and marketing, among other things — through the adoption of task automation, digitisation and migration to the cloud.

The application of artificial intelligence, super computing power and analytics can further turn massive amounts of data into useful information that will enhance the company’s ability to compete more effectively.

For instance, collecting and analysing data on shopper purchases will offer insights that help businesses tailor more effective (even customised) future sales, marketing and promotions. Meanwhile, predictive data can lower repair expenses and costly downtime at production lines.

For production, the switch to greater mechanisation, automation, robotics and internet of things can also enhance productivity — for example, by reducing human error and wastage.

To summarise, we address the supply side of the equation — production — through a multi-pronged approach. Firstly, we must reinvigorate private-sector investments with the government in the key role as catalyst, facilitator and enabler.

Productivity can be enhanced through digital transformation. To accelerate the adoption of digitalisation, the people must be effectively trained and equipped with the necessary digital skills.

Critically, Malaysia must undertake structural reforms of existing ecosystems. We have included four case studies (see sidebars) where restructuring can result in greater productivity — that is, growth without unnecessary cost inflation, thereby leading to lower overall prices.

Raising production — more for less

If all of these — and more — can be achieved, Malaysia can raise production output with a less than proportionate increase in investments. This would kick-start a new virtuous cycle (see Chart 10).

Higher productivity translates into lower costs and higher profits for businesses even as average selling prices are lowered. There will be more money for reinvestments. New, and higher-paying, jobs would be created, translating into higher per capita incomes for the people.

Meanwhile, increased productivity and competitiveness in the global market translate into higher exports and larger trade and current account surpluses for the country — and stronger purchasing power for the ringgit, thereby lowering the cost of living.

Consumption can grow anew, only this time, the growth will be sustainable along with an improving standard of living.

Case study 1: Reimagining the financial services sector

Why did investments drop so sharply in the aftermath of the Asian financial crisis?

The 1997/98 crisis was a huge shock that exacted a heavy psychological toll on all, including businesses, the government and central bank as well as the people. It left lingering scars on both the political and economic landscape of the country.

We witnessed increased risk aversion in banks as well as on the part of regulators, as evidenced by rigid guidelines on provisions, risk weightage, coverage ratios and foreign funding, among other things.

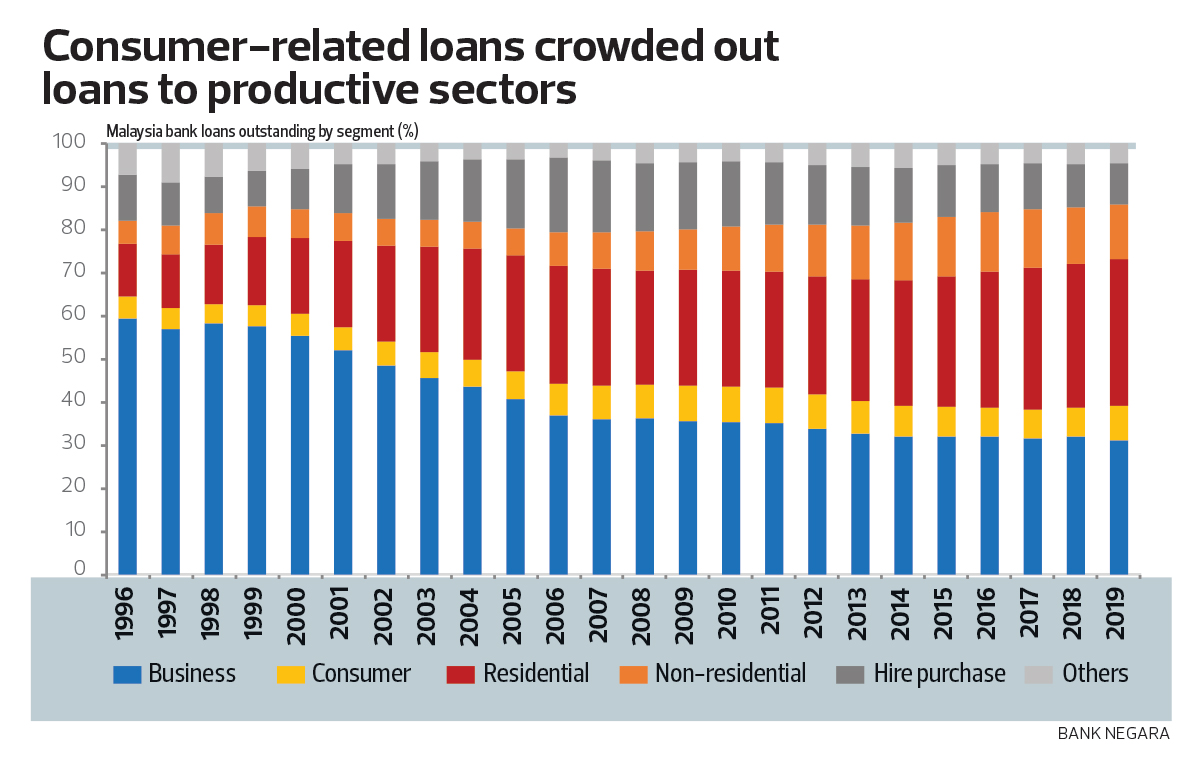

The ensuing banking-sector consolidation reduced the number of banks, leading to lesser diversity in terms of lending strategies and practices. All of the remaining big banks gravitated towards the safest segments — mortgage, hire-purchase loans, personal loans and credit cards. Business loans were mostly directed to large, well-established companies where the perceived risks were low.

In particular, the sharp rise in mortgages crowded out loans to other productive sectors. Residential property loans grew 12.4% annually since 1996, well outpacing the banking sector loan growth of 7.5% over the same period. The share of mortgages as a percentage of total banking loans tripled from 12% to 34% from 1996 to 2019.

This has yet to even take into account the overbuilding of commercial and retail properties. Vacant office space, shoplots and empty shopping malls are all low productive assets, the same as unsold and unoccupied homes.

On the other hand, micro and small and medium enterprises (SMEs) with little financial data and hard assets for collateral have limited funding options. The same goes for start-ups, thereby constricting entrepreneurship and innovation, and potentially robbing the economy of growth with the highest productivity.

To stimulate new and innovative investments, deeper structural changes to the current financial system are needed — beyond moral suasion for existing banks to lend. After all, banks are private entities looking out for their bottom lines.

How do we address the issue of funding and banks’ risk aversion? The simple answer is data.

Risk is a function of the unknown, the uncertainties. The less we know of a project or business, the higher the risks and the greater the reluctance to finance it. Therefore, the answer must logically be to reduce the unknown — by collecting massive amounts of data, public and private, and consolidating it within one digital platform, and through the use of supercomputing power, artificial intelligence and analytics, to transform the data into useful information. The more information, the lower the risks.

Availability and accessibility to information should, in turn, promote a more robust ecosystem and innovative lending, such as community crowdfunding. The ecosystem must include not just traditional banks but also digital banks and fintech companies. Of course, the government must facilitate this with the relevant regulations.

The tremendous growth of fintech companies such as Ant Financial (an associate company of Alibaba Group Holding) in China and Square in the US are proof of concept. These companies have very successfully cultivated and helped grow a generation of micro and small businesses by knowing their customers in ways that traditional banks cannot — through the amassing of massive amounts of data.

Data is the most powerful currency in the digital future. A robust shared data platform will not only transform the financial sector but also, we foresee, be the direct catalyst for changes across a broad swathe of industries.

Case study 2: Ease of doing business biggest impediment to investments

The key to attracting fresh investments is clearly the ease of doing business itself. One of the major considerations when companies select the location of their investments is the level of red tape and the associated compliance costs.

It is almost inevitable that the number of rules, regulations and procedures drawn up by bureaucracy increases over time — unless there is a conscious effort on maintenance, such as discarding those that become irrelevant due to technology or process changes. And when you add the multiple layers of authorities, from federal to state governments to local district councils, the totality of red tape can be so daunting that it deters new investments altogether.

The solution is to cut through the bureaucracy. Obviously, there are a lot of vested economic interests at stake. Therefore, to instil confidence, the framework and execution must be clear and transparent.

For starters, most existing requirements and processes can be migrated online and consolidated into a single one-stop platform. This will not only make submissions more convenient for businesses, it will improve timeliness and eliminate duplication.

More critically, by publicly disclosing all the regulations, requirements and criteria, there is transparency, consistency and certainty. Businesses know exactly what the qualifications needed are and can self-assess their eligibility.

1. Since there is already a set of subsidiary legislation — rules and regulations that do not require parliamentary approvals — in existence, for the first cut, allow a two- to three-month timeline for every agency and authority to confirm their relevance. Those not reconfirmed will be deemed to have lapsed and are no longer applicable. . This is necessary as red tape almost always grows over time. Think of your house and why clutter accumulates. It is easier to find new places to store stuff than to painstakingly go through old stuff and decide if they will ever be used again. We bet the only time this happens is when you move house!

2. To ensure regular maintenance and relevance, every new rule, regulation and guideline should have an expiry date, up to a maximum of, say, three years. Unless it is renewed, with justifiable reasons, it lapses. And as a guide, only 70% of existing regulations can be renewed.

3. In areas where it is highly technical, such as meeting fire requirements for buildings, environmental requirements or water quality, professional firms can take on the responsibility of assessment. The authority need only perform random checks for compliance.

4. Set a maximum timeline for a decision on each application. For instance, any application not rejected within six months will be deemed approved.

5. When an application is rejected, the relevant authorities are required to state the reasons.

We suspect that by clearly listing out all the requirements of each district and state on a common platform, the spirit of competition will lead to self-induced streamlining and simplifying of the processes.

India’s move towards a digitally-enabled policy initiative is an excellent example of how getting permits and approvals can be transformed by digitisation and associated structural reforms. It contributed to a significant shift in the country’s ranking in the World Bank’s Ease of Doing Business index. In the latest 2020 report, India is ranked 63rd among 190 nations, up from 77th in 2019 and 142 in 2015.

Chart 1 ranks the perception of the Malaysian government’s ability to formulate and implement policies and regulations that are conducive to private-sector investments. We are ranked well below Singapore, South Korea, Japan, Taiwan and Hong Kong. In fact, our regulatory quality as defined by the World Bank has deteriorated since 2014.

Tables 1 to 3 compare the time and documentation required for cross-border trading for Malaysia, Singapore and South Korea. Undertaking an import-export business in Malaysia clearly requires more documentation and a longer timeline for compliance.

Chart 2 outlines the myriad submissions and approvals — from the district council, state and federal governments — required for a typical housing development project. It takes more than 18 months, on average, from land conversion to project launch, before actual construction can even begin.

Case study 3: Pay for training programmes only upon job placement

Human capital is the most valuable resource of a country. However, Malaysia is not fully maximising this productive capacity.

For instance, while the overall unemployment rate was relatively low at 3.4% (pre-pandemic), unemployment among the young is high — 15.4% for those in the 15-19 age group, 9.6% for those in the 20-24 age group and 3.9% for those aged 25-29. And this is an underestimation, as many unemployed are not registered.

Transition to the digital economy will displace many existing jobs, owing to increased automation and mechanisation. These displaced people will need different skill sets for newly created jobs.

Also, existing workers will increasingly be required to possess a certain degree of digital skills as businesses embrace the digital transformation. The shift to higher-value and more capital-intensive industries and a reduction in reliance on cheap foreign labour require upskilling and reskilling for Malaysians.

There are many government funded-subsidised education and training programmes. However, most are not effective and only to capitalise on government funding. According to various studies done, including by Khazanah Nasional and World Bank-Talent Corp, many graduate-trainees remain unemployed after passing out because they continue to lack the skill sets employers require — such as soft skills like communication and analytical skills, critical-creative thinking, digital skills as well as work experience. How do we change this?

Simple. The education and training curricula must be tailored to meet current and future market demand. And we ensure this by packaging training programmes such that payment is only made after the graduate successfully secures a job.

This would force training academies to work closely with all prospective employers — small and large businesses, multinational corporations as well as the public sector — on the type of jobs that are available and the skill sets required for these jobs.

Academia must actively work with the industry on internship programmes — to provide trainees with on-the-job experience — and career services for eventual job placements.

To raise the probability of successful job placements, training academies must also carry out stringent assessments on the suitability of applicant trainees at the outset — and guide them towards the best career paths based on their individual profiles.

This proposed structure will ensure that all graduates have the necessary skill sets required in an evolving job market and that they will be able to successfully secure jobs for which they are trained and can therefore, command the appropriate wages.

Putting every able and willing worker to work will raise the country’s productive capacity and potential production growth without causing unnecessary wage inflation.

Case study 4: Boost home affordability with a more efficient property ecosystem

Owning a home is the aspiration of every Malaysian. But the relentless rise in home prices, which has far outpaced income growth, is increasingly putting home ownership beyond the means of the average person or sending households into unsustainable indebtedness.

In particular, home prices have risen rapidly since 1990, fuelled by historically low interest rates and enabled by the then government’s policies (such as home ownership campaigns, Developer Interest Bearing Scheme and a reduction in the real property gains tax) and banks’ aggressive lending for mortgages. As a result, home affordability has declined by half.

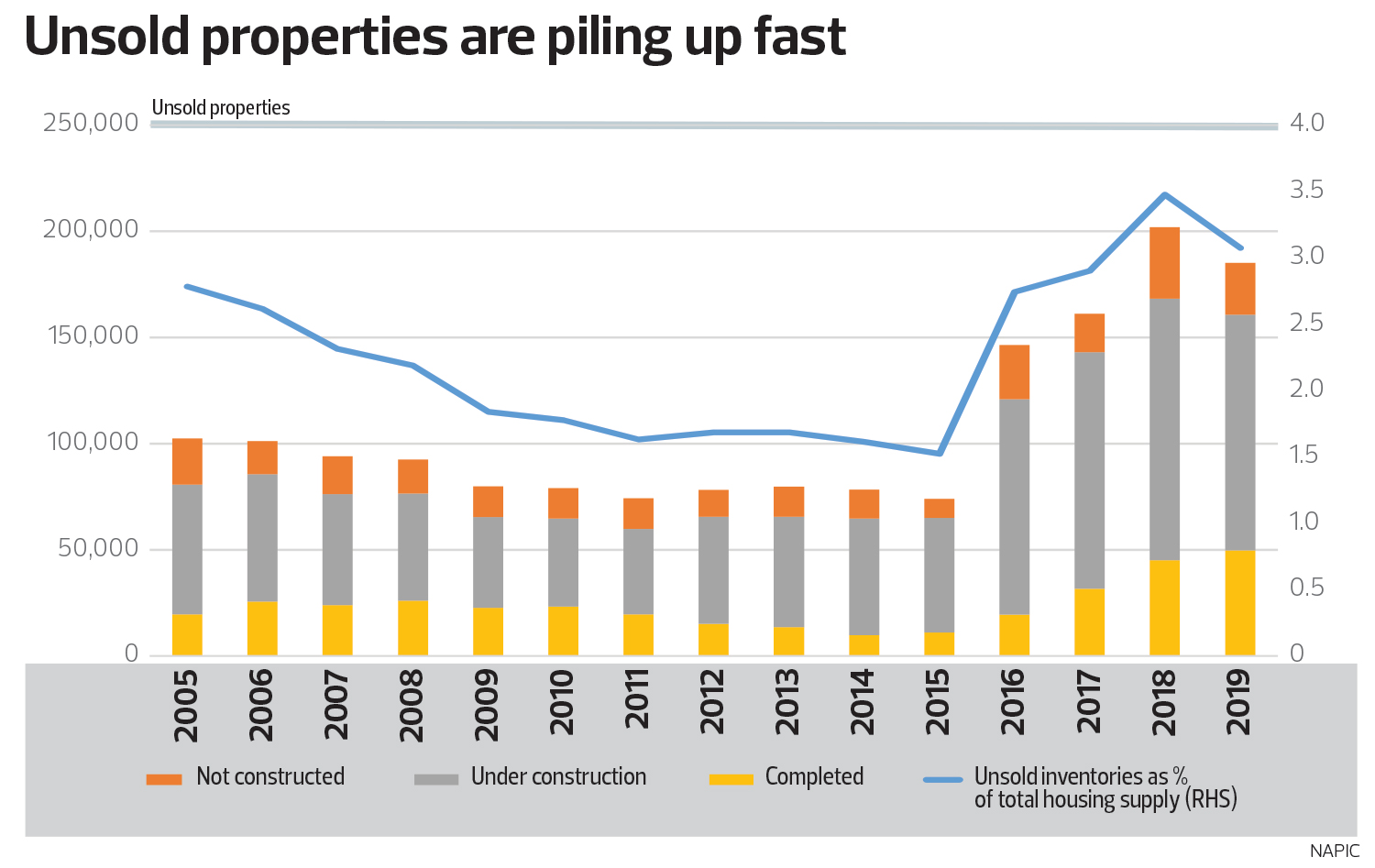

At the same time, rising home prices and profit margins have led to a building boom by property developers. Persistent overbuilding coupled with the increasing unaffordability of homes is creating an untenable rising pile of unsold properties that is also tying up precious resources as unproductive assets.

(For a more detailed discussion, please refer to our previous article entitled “What ails the Malaysian residential property sector”, The Edge Singapore, Issue 940, July 6).

The primary purpose of housing to society is to provide shelter or a home for individuals and families. The property sector is, at the same time, a major contributor to economic activity, employment and tax revenue.

Like the financial services industry, we believe the property sector requires wholesale changes to the eco-structure and system to resolve its current predicament.

Singapore is an interesting case study. The country has one of the most expensive private housing markets in the world. A stately colonial bungalow goes for more than $200 million.

Yet, it also boasts one of the highest home ownership rates in the world, attributed to the success of the Housing Development Board (HDB). The government builds affordable housing for the people, subsidised by the sale of land at high prices to the private sector. Eighty per cent of Singaporeans now live in a government-built (HDB) flat. HDB projects are well-designed and maintained, resulting in significant home equity gains over time.

This is a good example of a successful income-wealth redistribution initiative aimed at reducing inequality. One can clearly see the stark contrast between Singapore and Hong Kong, another country where land and property prices are among the highest in the world. In the latter, the property market is controlled by a handful of private developers. Home ownership stands at just 49.2% and rising home unaffordability contributes to a skyrocketing cost of living, all of which are part of the root causes of the recent social unrest.

That said, we see Singapore as a unique case. Because land accounts for a huge portion of total property costs, as high as 70%, it gives the government substantial leverage for its subsidised public housing programme. A similar programme would be far less effective in Malaysia, where land typically accounts for only about 15% of gross development value. Thus, subsidising land cost can only very marginally lower home selling prices.

Indeed, Malaysia has tried for years to bring down home prices, from controlling the cost of land and materials as well as construction — for instance, the use of prefabricated modular construction or an industrialised building system — to moral suasion and mandatory building of “low-cost homes”. All these measure have had limited success. Absolute and psf prices for homes continue to rise.

Worse, most of these low-cost homes are being built in farther and farther-off locations, making commuting to work difficult, especially for lower-income households dependent on public transport.

Lowering costs by cutting amenities, facilities and surrounding infrastructure and/or building homes so small in size and in high density that they ultimately destroy homeowner equity is clearly not the answer. A case in point — PR1MA homes have low take-up rates and limited success despite billions of ringgit having been spent on them.

Persisting with these same old ideas — building low-cost homes, extending mortgage tenures, giving concessions on taxes and duties — as solutions is simply not going to work. To quote Albert Einstein, “The definition of insanity is doing the same thing over and over again, but expecting different results.”

It is high time Malaysia tried another approach, one that will simultaneously address the growing home affordability issue — by lowering home prices — and rejuvenate the sector as well as minimise future systemic risks from property’s cyclicality.

The price of a home to the buyer is made up of the tangible costs (land, materials, construction, compliance, sales and marketing expenses, among other things) plus profits for the property developer, suppliers and contractors and the financing bank.

The required return for any investment is a function of risks. The higher the risks, the higher the required returns (profits) and vice-versa.

Right now, the developer puts in upfront capital to build and risks selling less than the required number of homes to break even. When this happens, suppliers and contractors risk not being able to collect their dues. The bank faces the risk of loan defaults by both the developer and the buyer, who ends up with a half-completed home if the project is abandoned.

All these risks — most of which occur during the three-year construction period — have to be compensated. And they add up to a higher price for the home, in the form of a higher required rate of return for the developer, suppliers, contractors and bank.

The obvious solution is to remove the risks and therefore, reduce the required returns (profits) — by changing the ecosystem.

1. The developer is allowed to withdraw the project and fully refund deposits if confirmed sales (with secured mortgages) are less than 70% within a specified period, say six months from launch.

2. The project goes ahead upon hitting the minimum sales threshold. The bank will provide a bridging loan to the developer to build.

3. The bank takes on a more active role in project oversight. Progress payments will be released directly to suppliers and contractors upon verification by its appointed quantity surveyor.

4. Upon completion of the project, the developer will receive its profits and cash from the bank.

5. The mortgage will be drawn down and the homeowner will start repayment upon handover with certificate of fitness (CF).

In this ecosystem, there is no risk of project failure for the developer and the upfront capital requirements are smaller. The suppliers and contractors will be guaranteed timely progress payments from the bank. For the bank, there is no risk of developer loan default due to the project being abandoned, overpayments for supplies and/or fraud.

Last but not least, the buyer does not get saddled with an uncompleted home for which they will still have to make mortgage repayments. Plus, under the new structure, they do not have to service the mortgage until the home is ready for moving into, which means no double costs as many will likely be paying rental during the construction of their new homes.

Lower risks and required returns for all stakeholders equal lower costs and home prices — and improved affordability for young Malaysians. It is a win-win situation for all parties involved.

This is in fact not a novel concept. Similar models are already being used — and have proven successful — in developed countries, including the US, Canada and Australia. Why not learn from them, and refine and adopt the concept to suit our own purposes and objectives, for the better of all?

The above will effectively lower house prices and improve affordability. However, on its own, it is still not sufficient. Many Malaysians simply do not have enough even for the upfront deposit, due to a combination of factors including low per capita income, excessive consumption and high household indebtedness.

As the solution to this revolves around financing instead of addressing the supply side, we will leave further discussion to a later article.

"consumption" - Google News

August 06, 2020 at 03:00PM

https://ift.tt/33BrN2b

Special Report: Pivoting from consumption to production - The Edge Markets MY

"consumption" - Google News

https://ift.tt/2WkKCBC

https://ift.tt/2YCP29R

Bagikan Berita Ini

0 Response to "Special Report: Pivoting from consumption to production - The Edge Markets MY"

Post a Comment